This Week's EchoVector Pivot Point Charts and Analysis And Active Advanced Position Management OTAPS-PPS Approach For The Gold Metals Market: 2/25/14

BY KEVIN JOHN BRADFORD WILBUR,

Chief Market Strategist And EchoVector Methodology Analyst

ADVANCEVEST AND PROTECTVEST BY MOTION DYNAMICS AND PRECISION PIVOTS

Chief Market Strategist And EchoVector Methodology Analyst

ADVANCEVEST AND PROTECTVEST BY MOTION DYNAMICS AND PRECISION PIVOTS

BACKGROUND: LAST YEAR IN REVIEW

Last year the dramatic decline in gold prices that occurred since the fall of 2012 was big news. Fortunately, in November of 2012 I alerted the gold market to what then was a cyclically important week in gold. The two weeks of trading that followed proved to be of great interest to participants worldwide. The price of gold fell significantly, trading down from around $160 on the GLD ETF to a low just below $151, a fall of over 5.5%.

I reiterated the importance of this same cyclical week a quarter later in my article of February 11, 2013, titled "Gold Chart: Cyclically An Important Week In Gold". That cyclical week proved important again indeed. So much so that, in late February of 2013 (this week a year ago), amidst a plethora of bullishly speculative articles, and when gold was bouncing off a seeming near-term bottom, and when many analyst where again filled with risk-on enthusiasm for the precious metal, I instead suggested that regardless of the relative price level of gold at that time, a more prudent strategy likely was to enter gold closer to the end of June 2013 for a seasonal bounce. See "Gold Chart: Price May Be Right, But Is Timing?"

Well, I couldn't have been more correct. Gold incurred a massive leg down in April of 2013.

Encountering again significant gold risk-on enthusiasm at these new lower price levels. In May of 2013 I elected to put out a third article on gold titled, "Gold Charts: Warning In February Still Valid Today". In that article I warned that last year's then seasonal down-pressure was still likely not over. The wisdom of February's article had become fully apparent, with gold prices down another 20%, and the GLD falling near $131. In May's article I reiterated the importance of waiting patiently for the end of June to find a positive risk-reward re-entry time-point for gold, based on advanced echovector analysis. Another final leg down was forecast in May. As things ended up, it would have been hard for me, and for the echovector analysis approach to have been more correct, with gold falling further in June 2013 to a closing low on the GLD the week of June 27TH below $116. Meeting both my price and timing targets then, I issued a major buy signal alert consistent with these article's analysis and forecasts.

As forecast and warned early last year, the first half of 2013 proved to be an historic sell-off in gold prices. My model had indicated the strong seasonal buy signal at the end of June 2013 early on. And the bottom did come in on June 27TH, the week it was forecast due, and given with clear notice of a possible bounce back to the $135 area into September, but also with clear notice and with a warning again going forward from there into the end of the year, This was all also all published at the respective "Market Alpha Newsletter Group" newsletters and websites,goldinvestorweekly.com and goldpivots.com, and at my EchoVector Analysis webpage at seekingalpha.com

The 2013 gold metals EchoVector Analysis forecast unfolded right on target. In August I reiterated notice of the possible bounce back to the $135 area into September, and also reiterated warnings that the risk-reward ratio to any such risk-on positions would begin to increase dramatically the week of September's primary options on an annual echovector perspective basis. I also presented analysis to this effect. This can be found in the August 2013 articles "As In Previous Quarters, This Is A Very Important Week In The Gold Market" and "Today Is An Important Day For Gold", as well as in additional posts published atseekingalpha.com and goldinvestorweekly.com and goldpivots.com in August that year.

On September 5TH of 2013, believing the better part of the season bounce was coming mature, I also published my article "Watch Out On Gold" alerting investors and trader's to specifics on how to interpret ensuing gold price motion mechanics, and when to exit the seasonal bounce using these, and when to reverse their short term longs back to shorts, and showed how nothing had changed regarding gold moving out of its "strong downward annual echovector momentum" that had been active into its low in the summer, and showed that these lows could easily be revisited before the year's end once again on an EchoVector Analysis basis.

On December 19TH 2013 I issued my final reversal Alert for 2013, calling for a bounce in gold into mid-January, and then possibly beyond. I believed such a short-term bounce could and should be positioned into on a trading basis at the very least. But also positioned into because of the possibility that gold might find longer term Presidential Cycle EchoVector support in 2014, and that this support might not necessarily materialize at lower absolute price levels. As it turned out, I was correct, and gold metal prices have moved forward very nicely since the Alert at the $115 level in December on the GLD ETF gold metals proxy price equivalency basis.

FORECAST: FORWARD INTO THIS YEAR

On January 12TH 2014, when the GLD had moved forward and closed just above the $120 level, I published my article "Revisiting Gold...", featuring a then current look at the charts.

In the article I emphasized how following EchoVector Analysis chart updates from both February and August 2013 on the GLD ETF, which illustrated how waiting until the end of June, had been a very good annual risk-on risk-management strategy for gold since July 2009.

The charts also indicated promise regarding a possible presidential cycle echo year in 2014 to its echobackyear of 2010 four years earlier, and how early February and late July/early August both proved to be significant inflection points in gold's price direction in 2010, and how a close watch in those periods in 2014 would be prudent as well.

The late July/early August inflection point had also proved to be once again active and significant in 2012, within the subsumed and in phase congressional cycle within this presidential cycle, which is also significant. It has also continued to prove operant in each of the subsumed annual cycles within this presidential cycle as well, which is further significant.

I also mentioned how those individuals who have been following the EchoVector Analysis Model alerts, and positioning in a manner consistent with its double-double leverage approach -- which utilizes related ETF Ultras and margin for extra leverage and multiples -- are very likely extremely happy with the 2013 EchoVector Analysis forecasts and advanced position management outcomes. I also mentioned at that time that such investors and traders were double-double long gold at the GLD ETF $114.55 proxy price equivalency basis, and had been so since the week before Christmas 2013, based on the major EchoVector Analysis OTAPS-PPS strategy and position management alert issued in late December 2013. And they might even had been more aggressively (and even more profitably) long having used even more advanced derivatives management position strategies.

I also highlighted how important a time it was from an EchoVector Analysis Perspective for gold metals prices going forward into January's primary option expiration, and how important it was going forward into the following three week's from there also.

Last year, as well as the last several quarters, the period following the January quarterly option's expiration cycle did little in forwarding gold metals price levels, and actually proved quite precarious to prices into the first week of the following month, and in some instances, more so even beyond. However, the power of the 4-year presidential cycle echovector and the 2-year congressional cycle echovector could easily trump nearer term quarterly patterns that accrued during the recent down-pressure period.

Because of this risk, I suggested positive caution going forward, and the application of advanced triggered OTAPS switching applications in current open position management. For context see the following chart. Corresponding analysis, strategy, and position management protocols were also discussed.

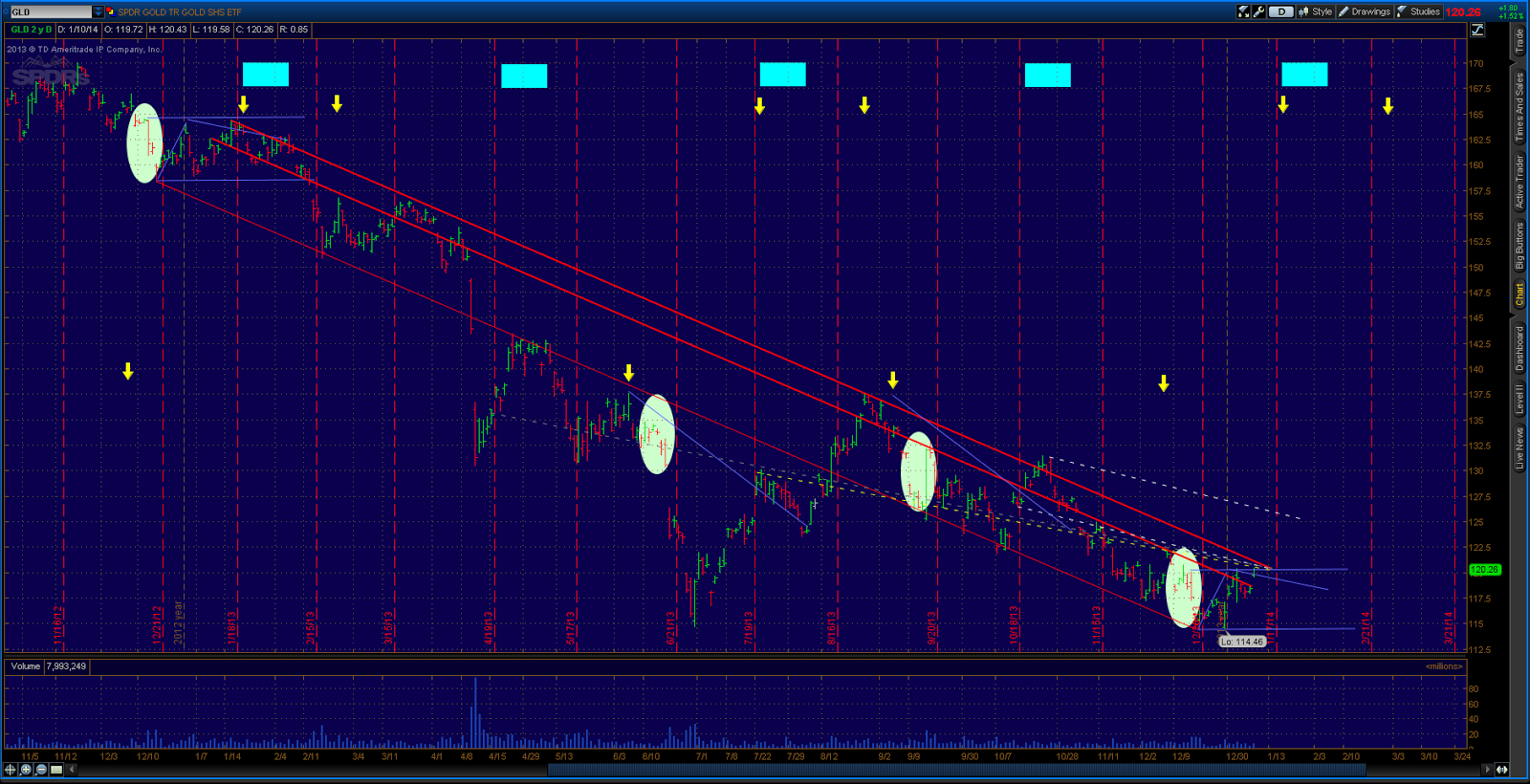

GLD ETF 1-YEAR DAILY OHLC

ANNUAL CYCLE ECHOVECTOR ANALYSIS PERSPECTIVE

DECEMBER 2012 TO DECEMBER 2013 FOCUS

(Click to enlarge)

In the chart above the horizontal blue-purple extension vectors running about 2 months worth of trading days long from the light green oval areas in December of 2013 and December of 2012. The lower horizontal price level and time period following December of each year represents the currently active lower threshold OTAPS-PPS price level target switch, and the upper horizontal price level represents the upper threshold OTAPS price level target switch. Price movement up through the upper threshold generates a double-double open long at that trigger price and time. Price Movement down through the upper threshold closes any open long positions and generates a double-double open short position at that price and time. Directional tick is very important here. Effective directional position polarity switching can also be accomplished by setting the effective open and/or close trigger prices one cent on either side of the initial base target trigger price threshold.

Additionally, movement down through the lower threshold OTAPS trigger switch closes any long positions that may otherwise be open, and generates a double-double open short position. Price movement up through the lower threshold switch will close any short position that may be open and generate a double-double long position open. The double-double leverage positions can be accomplished by utilizing related and highly liquid gold metals ULTRA ETF's on margin.

The $120.25 GLD proxy price equivalency level and echovector pivot point and otaps-pps upper band switch level was particularly important. On one side of the switch, gains from the $114.55 level were locked in. On the same side of the switch additional gains could be accrued in case of a rally. While having been penetrated upwards, further gains could also be accrued upon re-penetration to the downside in case of market price weakness. As it turned out, the bias in favor of the presidential cycle echovector and the congressional cycle echoVector for relative strength right up into the last week of February occurred. And this proved very profitable for adherents to the analysis and to the active position management strategy discussed. See the chart below.

GLD ETF 4-YEAR DAILY OHLC

PRESIDENTIAL CYCLE ECHOVECTOR ANALYSIS PERSPECTIVE

(Click to enlarge)

ECHOVECTOR ANALYSIS FRAMECHARTS, STRATEGY, AND THE WEEK AHEAD

This brings us to the following question, "Is it time for caution; that is, is it time for position cover or even time for position polarity reversal now that momentum lift into this part of February has been fulfilled? We have collected $15 on the GLD, over 13%, and about four times that on an open double-double position, over 50% in about 2 months!

Does the positive price lift from the December lows to current price levels portend further strength ahead this year, and should we think about adding to our position, and not trimming back?

Reviewing the chart above, we see that the bias on the active presidential cycle echovector (white), the congressional cycle echovector (yellow), the annual cycle echovector (shorter white), and the bi-quarterly cycle echovector (shorter yellow) from Tuesday's close leading to each of their respective echobackdates does not appear to support near-term relative strength.

The blue extension otaps-pps position polarity switch signal vectors transposed from the forward pivot point cluster in 2010 to the corresponding echo-forward dates in 2014 provide a formal forward analytical context for symmetrical support and resistance pricing and timing indicators and position polarity switching actions moving forward through the quarter of 2014 into the middle of May, given present presidential cycle echovector momentum. We can identify relative price momentum weakness going into and through many of this March's equivalent periods from the echobackdates of the key echovector cycle lengths we have been examining. For this reason it would be prudent to utilize the key active otaps-pps position cover and position polarity reversal vector highlighted on the chart above. This puts the otaps-pps position cover and/or position reversal price trigger this week at around the $129.30 GLD ETF proxy price equivalency basis level for the gold metals market. Staying above this price, or moving down through it and then back up through it, positions net long gold. Moving down through this price closes long position at it and opens up short below it. See the zoomed chart below.

GLD ETF 4-YEAR DAILY OHLC

PRESIDENTIAL CYCLE ECHOVECTOR ANALYSIS PERSPECTIVE

CHART ABOVE ZOOMED TO FIRST FIVE MONTHS OF 2014

(Click to enlarge)

This active advanced position management strategy will enable us to capture and consolidate our well-earned capital gains from late December 2013 while positioning us to take advantage of both further price gains or sudden cyclical price weakness in the gold metals market. When using this strategy it is important to remember to update and regularly adjust the key active echovectors the otaps-pps active advanced management position adjustment switch signal trigger symmetry transposition is based on. EchoVectors and OTAPS-PPS Position Polarity Cover And Switch Signal Vectors are powerful and advanced and very effective, but also very fluid calculations. It is important to keep up with them.

For information on calculating echovectors, coordinate forecast echovectors, and echovector pivot points yourself, see "The Simple Single-Period EchoVector Pivot Point Calculation."

Thanks for reading, and godspeed in your gold market investing and trading.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long or a short position in GLD and/or related Ultra ETF's over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Kevin John Bradford Wilbur is the Chief Market Strategist and Senior EchoVector Analysis Methodologist at PROTECTVEST AND ADVANCEVEST. He is a prize-winning Economist and Financial Physicist with an over 35 year span of experience and awards in Academics, Research, Management, Practice and Trade. Kevin has specialized experience in the major market indexes, commodities, ETFs, emini-futures, and in derivatives and the derivatives markets.

See echovector.info and http://seekingalpha.com/author/kevin-wilbur

This article is tagged with: Gold & Precious Metals

ECHOVECTOR CYCLE LENGTH COLOR CODE GUIDE:

4-Year Presidential Cycle EchoVectors: White

2-Year Congressional Cycle EchoVectors: Yellow

1-Year Annual Cycle EchoVectors: White or Red

6-Month Bi-Quarterly Cycle EchoVectors: Yellow

3-Month Quarterly Cycle EchoVectors: White

OTAPS-PPS Position Polarity Cover And/Or Position Polarity Switch Signal Time/Price Vectors Extending From Key Coordinate Forecast EchoVector Pivot Points: Blue-Purple

Kevin John Bradford Wilbur is the Chief Market Strategist and Senior EchoVector

Analysis Methodologist at ADVANCEVEST. He is a prize-winning Economist and

Financial Physicist with an over 35 year span of experience and awards in

Academics, Research, Management, Practice and Trade. Kevin has specialized

experience in the Major Market Indexes, Commodities, ETFs, and in derivatives

and the derivatives markets. See echovector.info and

http://seekingalpha.com/author/kevin-wilbur

Analysis Methodologist at ADVANCEVEST. He is a prize-winning Economist and

Financial Physicist with an over 35 year span of experience and awards in

Academics, Research, Management, Practice and Trade. Kevin has specialized

experience in the Major Market Indexes, Commodities, ETFs, and in derivatives

and the derivatives markets. See echovector.info and

http://seekingalpha.com/author/kevin-wilbur

METHODOLOGY FOOTNOTES

"EchoVector Theory and EchoVector Analysis assert that a securities prior price patterns may influence its present and future price patterns. Present and future price patterns may then, in part, be considered as 'echoing' these prior price patterns to some identifiable and measurable degree.

EchoVector Analysis is also used to forecast and project potential price Pivot Points (referred to as PPP's --potential pivot points, or EVPP's --EchoVector Pivot Points) and active, past and future coordinate forecast echovector support and resistance echovectors (SREV's) for a security from a starting reference price at a starting reference time, based on the securities prior price pattern within a given and significant and definable cyclical time frame.

EchoVector Pivot Points and EchoVector Support and Resistance Vectors are fundamental components of EchoVector Analysis. EchoVector SREV's are constructed from key components in the EchoVector Pivot Point Calculation. EchoVector SREV's are defined and calculated and also referred to as Coordinate Forecast EchoVectors (CFEV's) to the initial EchoVector (XEV) calculation and construction, where X designates not only the time length of the EchoVector XEV, but also the time length of XEV's CFEVs. The EchoVector Pivot Points are found as the endpoints of XEV's CFEVs' calculations and the CFEVs' constructions.

The EchoVector Pivot Point Calculation is a fundamentally different and more advanced calculation than the traditional pivot point calculation.

The EchoVector Pivot Point Calculation differs from traditional pivot point calculation by reflecting this given and specified cyclical price pattern length and reference, and its significance and information, within the pivot point calculation. This cyclical price pattern and reference is included in the calculations and constructions of the echovector and its respective coordinate forecast echovectors, as well as in the calculation of the related echovector pivot points.

While a traditional pivot point calculation may use simple price averages of prior price highs, lows and closes indifferent to their sequence in time to calculate its set of support and resistance levels, the echovector pivot point calculation begins with any starting time and price point and respective cyclical time frame reference X, and then identifies the corresponding "Echo-Back-Time-Point" within this cyclical time frame reference coordinate to the starting reference price and time point A. It then calculates the echovector (XEV) generated by the starting reference time/price point and the echo-back-time-point, and includes the pre-determined and pre-defined accompanying constellation of "Coordinate Forecast EchoVector" origins derived from the prior price pattern evidenced around the echo-back-time-point within a certain pre-selected and specified range (time and/or price version) that occurred within the particular referenced cyclical time-frame and period X. Security I's EchoVector Pivot Point constructions then calculate and project the scope relative echovector pivot points that follow A, and the support and resistance levels determined by the ensuing coordinate forecast echovectors and their selected range definition inclusion (fully differentiating the time-sequence of the origins), the cyclical time-frame X, and to XEV's slope.

EchoVector Pivot Points are therefore advanced and fluid calculations and effective endpoints of projected coordinate forecast echovector support and resistance time/price levels, projections that are constructed from and follow in time from the starting reference price, time/price point A (echovector endpoint) of the initial subject focus echovector construction, and which occur within an EchoVector Pivot Point Price Projection Parallelogram construct: levels which are derived from coordinate (support and/or resistance) forecast echovectors calculated from particular 'scope and range defined' starting times and price points reflecting the time and price points of proximate scale and scope and time/price pivoting action that followed the initial subject focus interest echovector's echo-back-date-time-price-point B (derived from and relative to the initial subject focus echovector's starting time-point and price-point A, and the echovector's given and specified cyclically-based focus interest time-span X, and the initial subject focus echovector's subsequently derived slope relative momentum measures).

The EchoVector Support and Resistance Vectors, referred to as the Coordinate Forecast Echovectors, are used to generate the EchoVector Pivot Points."

From "Introduction to EchoVector Analysis And EchoVector Pivot Points"COPYRIGHT 2013 ECHOVECTORVEST MDPP PRECISION PIVOTS

DISCLAIMER

This post is for information purposes only.

There are risks involved with investing including loss of principal. PROTECTVEST AND ADVANCEVEST BY ECHOVECTORVEST MDPP PRECISION PIVOTS and its Divisions and Subdivisions makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections presented or discussed by PROTECTVEST AND ADVANCEVEST BY ECHOVECTORVEST MDPP PRECISION PIVOTS and its Divisions and Subdivisions.

There is no guarantee that the goals of the strategies discussed by PROTECTVEST AND ADVANCEVEST BY ECHOVECTORVEST MDPP PRECISION PIVOTS and its Divisions and Subdivisions will be achieved.

NO content published by us on the Site, our Blog, and any Social Media we engage in constitutes a recommendation that any particular investment strategy, security, portfolio of securities, or transaction is suitable for any specific person. Further understand that none of our bloggers, information providers, App providers, or their affiliates are advising you personally concerning the nature, potential, value or suitability of any particular security, portfolio of securities, transaction, investment strategy or other matter.

Again, this post is for information purposes only.

Before making any investment decisions we recommend you first consult with you personal financial advisor.

IN ASSOCIATION WITH PROTECTVEST AND ADVANCEVEST

BY ECHOVECTORVEST MDPP PRECISION PIVOTS

Positioning for change, staying ahead of the curve,

we're keeping watch for you."

Friday, february 27, 2014

MARKET ALPHA NEWSLETTERS BY BRIGHTHOUSE PUBLISHING WITH ECHOVECTOR ANALYSIS, KEY ECHOVECTORS, ECHOBACKDATES, ECHOBACKTIMEPERIODS, COORDINATE FORECAST ECHOVECTORS, ECHOFORWARD DATES, ECHOFORWARD TIMEPERIODS, ECHOVECTOR PIVOT POINT PROJECTIONS, AND ACTIVE ADVANCED MANAGEMENT OTAPS-PPS POSITION POLARITY SWITCH SIGNAL VECTORS HIGHLIGHTED AND ILLUSTRATED

Publications with articles, posts, analysis, and commentary regularly utilizing, focusing on, presenting, and/or employing active advanced management forecast, trade, and position management methodologies and technology, including EchoVector Analysis:

For current applications of EchoVector Analysis see the following Fourteen market-oriented newsletters (free online) featuring EchoVector Analysis FrameCharts and OTAPS-PPS Active Advanced Position Management Forecast Price GuideMaps:

1. The EchoVector Market (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at echovectorvest.blogspot.com and marketinvestorweekly.com

The Market Pivots Forecaster

Free Online at echovectorvest.blogspot.com and marketinvestorweekly.com

The Market Pivots Forecaster

2. The ETF (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at etfpivots.blogspot.comand etftraderweekly.com and etfinvestorweekly.com

The ETF Pivots Forecaster

Free Online at etfpivots.blogspot.comand etftraderweekly.com and etfinvestorweekly.com

The ETF Pivots Forecaster

3. The E-mini Futures (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at eminipivots.blogspot.com and e-mininews.com andmarketinvestornews.com and marketinvestorweekly.com and market-pivots.com

4. The Dow Composite (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at dowpivots.blogspot.com

The Dow Pivots Forecaster

Free Online at dowpivots.blogspot.com

The Dow Pivots Forecaster

5. The S&P500 Composite (Price Pivots) Forecaster and Position Management Newsletter

6. The Nasdaq 100 Composite (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at qqqpivots.blogspot.com and marketinvestornews.com andmarketinvestorweekly.com and market-pivots.com

7. The Gold Metals (Price Pivots) Forecaster And Position Management Newsletter

By Gold Investor Weekly and Brighthouse Publishing.

Free Online at goldpivots.blogspot.com and goldinvestorweekly.com

The Gold Pivots Forecaster

Free Online at goldpivots.blogspot.com and goldinvestorweekly.com

The Gold Pivots Forecaster

8. The Silver Metals (Price Pivots) Forecaster And Position Management Newsletter

By Silver Investor Weekly and Brighthouse Publishing.

Free Online at silverpivots.blogspot.com and silverinvestorweekly.com

The Silver Pivots Forecaster

Free Online at silverpivots.blogspot.com and silverinvestorweekly.com

The Silver Pivots Forecaster

9. The Bond Market (Price Pivots) Forecaster And Position Management Newsletter

By Market Investor Weekly and Brighthouse Publishing.

Free Online at bondpivots.blogspot.com

10. The Oil Market (Price Pivots) Forecaster And Position Management Newsletter

By Market Investor Weekly and Brighthouse Publishing.

Free Online at oilpivots.blogspot.com

The Oil Pivots Forecaster

Free Online at oilpivots.blogspot.com

The Oil Pivots Forecaster

11. The Commodity Market (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at commoditypivots.blogspot.com

The Commodity Pivots Forecaster

Free Online at commoditypivots.blogspot.com

The Commodity Pivots Forecaster

12. The Dollar (Price Pivots) Forecaster And Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at dollarpivots.blogspot.com

13. The Currency Market (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at currencypivots.blogspot.com

The Currency Pivots Forecaster

Free Online at currencypivots.blogspot.com

The Currency Pivots Forecaster

14. The Emerging Market (Price Pivots) Forecaster and Position Management Newsletter

By Market Investor Weekly and BrightHouse Publishing.

Free Online at emergingmarket.blogspot.com

The Emerging Market Pivots Forecaster

Free Online at emergingmarket.blogspot.com

The Emerging Market Pivots Forecaster

SEE

MARKETINVESTORNEWS.COM, MARKETINVESTORWEEKLY.COM,ETFINVESTORWEEKLY.COM, ETFTRADERWEEKLY.COM,GOLDINVESTORWEEKLY.COM, SILVERINVESTORWEEKLY.COM, ECHOVECTOR.INFO,

AND

AND

AFFILIATE DOMAINS

DOWPIVOTS.COM, SPYPIVOTS.COM, QQQPIVOTS.COM,

GOLDPIVOTS.COM, SILVERPIVOTS.COM, OILPIVOTS.COM,

BONDPIVOTS.COM, DOLLARPIVOTS.COM, CURRENCYPIVOTS.COM,

COMMODITYPIVOTS.COM, EMERGINGMARKETPIVOTS.COM,

STOCK-PIVOTS.COM, MARKET-PIVOTS.COM,

ETFPIVOTS.COM, AND E-MINIPIVOTS.COM,

GOLDPIVOTS.COM, SILVERPIVOTS.COM, OILPIVOTS.COM,

BONDPIVOTS.COM, DOLLARPIVOTS.COM, CURRENCYPIVOTS.COM,

COMMODITYPIVOTS.COM, EMERGINGMARKETPIVOTS.COM,

STOCK-PIVOTS.COM, MARKET-PIVOTS.COM,

ETFPIVOTS.COM, AND E-MINIPIVOTS.COM,

Market Newsletter Weekly. Alpha Newsletter. Brand.

Special Notations

EchoVector Theory is a price pattern impact theory. EchoVector Analysis is an advanced technical analysis methodology. EchoVector Analysis is also presented as a behavioral economic application and securities analysis tool in price pattern theory and in price pattern behavior, study, and forecasting, and in securities analysis and price analysis and in securities price speculation.

EchoVector Pivot Points, special contributions to the field of technical analysis, are a technical analysis tool and application within EchoVector Analysis, and derived from EchoVector Theory in practice.

Kevin John Bradford Wilbur is the postulator of EchoVector Theory, the creator of EchoVector Analysis, and the inventor of EchoVector Pivot Points.

Copyright 2013 EchoVectorVEST MDPP Precision Pivots

|

PROTECTVEST AND ADVANCEVEST BY ECHOVECTORVEST MDPP PRECISION PIVOTS

Providing Forecasting and Trade Management Technology, Analysis, and Education Consistent With More Than Doubling the Portfolio Position Value of The Major Market (Dow 30 Industrials, DIA ETF) From Mid-2007 to Early 2009!... More Than Doubling Again from Early 2009 through 2010!... More Than Doubling Again in 2011!... More Than Tripling Again in 2012!... And More Than Tripling Agin in 2013! "Positioning for change, staying ahead of the curve, we're keeping watch for you!"

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.